No Filipino has done more to contain the economic impact of the pandemic and encouraged banks to do more for the common man

“I have said this before and I will say it again: We are one government. We are one Filipino nation.”

BSP has been and is ready to employ the necessary tools in its arsenal to address the impact of COVID-19 while staying true to its mandate.”

By Governor Benjamin E. Diokno

Bangko Sentral ng Pilipinas

When the gravity and magnitude of the pandemic first came to the fore, the Bangko Sentral ng Pilipinas acted swiftly and decisively to contain the economic fallout.

In this article, I detail the policy actions and extraordinary measures by the Philippine central bank to respond to the crisis in three parts, starting with an overview of our pandemic efforts, then looking back to structural reforms that were well underway even before then, and finally, trying to navigate what the future holds.

A crisis like no other

As early as February 2020 – before the first local transmission of the virus was even confirmed – the Monetary Board cut the policy rate by 25 basis points.

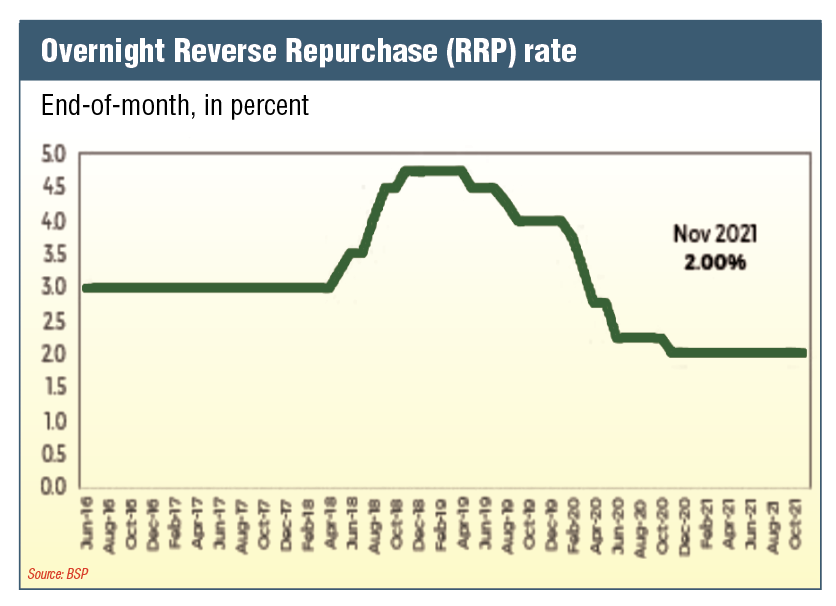

By the end of the year, the policy rate was cut by another 175 bps, bringing the cumulative reduction to 200 bps. From 4%, the key rate fell to a record low of 2%. The 2% policy rate was retained in our last meeting of the year to encourage private investment and consumer spending.

The reserve requirement ratio (RRR) was similarly reduced to increase the volume of loanable funds in the system.

For universal and commercial banks as well as non-bank financial institutions with quasi-banking functions, the RRR was cut from 14% to 12%, while the RRR for thrift banks was cut from 4% to 3% and from 3% to 2% for rural/cooperative banks.

.

Short-term rates kept low

At the same time, we calibrated our daily monetary operations to keep short-term rates low and support the effective transmission of the accommodative monetary stance to key financial variables.

We are slowly seeing signs of economic normalization as a result of our concerted efforts.

.

Beyond targeted policy interventions, the BSP implemented extraordinary liquidity measures to help fund the national government’s COVID response.

With the need to generate more resources to build healthcare facilities and vaccines urgently, we extended P540 billion in direct provisional advances to the national government. In addition, we remitted P23 billion in dividends in two tranches to augment the government’s pandemic war chest.

To date, our collective actions have injected P2.3 trillion in liquidity into the financial system. This is equivalent to nearly 13% of full-year nominal GDP.

These efforts were accompanied by a wide range of regulatory and operational relief measures for financial institutions.

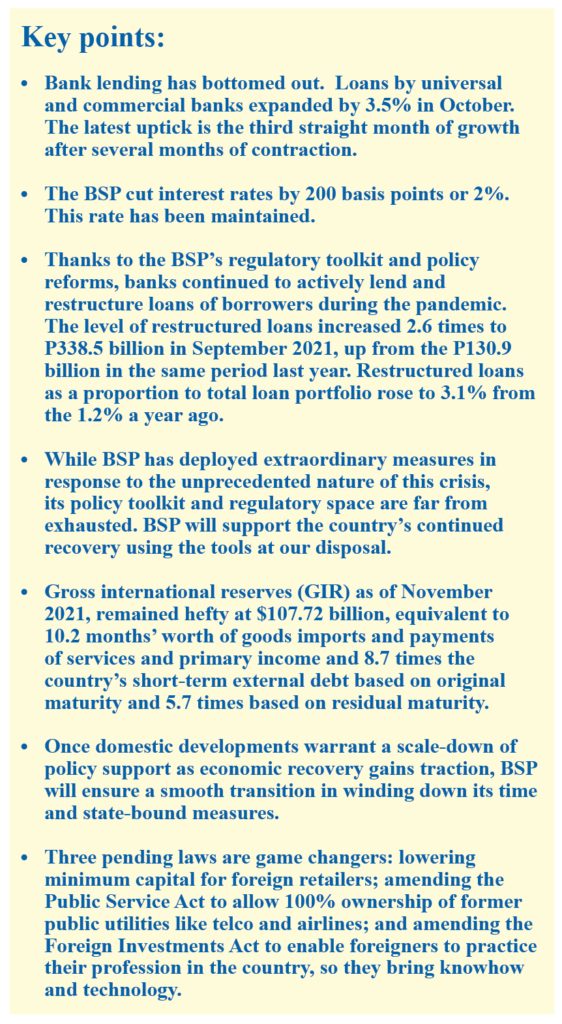

Bank lending appears to have bottomed out, with loans by universal and commercial banks expanding by 3.5% in October. The latest uptick marks the third straight month of growth after several months of contraction.

The effectiveness of our monetary interventions could also be seen in the sustained decline in domestic market interest rates. By September 2021, the benchmark 91-day T-bill rate fell by more than 200 basis points from January 2020.

Our monetary operations during the pandemic ensured that the supportive policy stance is transmitted to the economy.

Incentives for lending to MSMEs

Recognizing that small businesses were hard hit by mobility restrictions and lockdowns, we incentivized bank lending to MSMEs as compliance with the reserve requirement. In addition, the BSP temporarily increased the single borrowers’ limit and raised the ceiling for real estate loans of universal and commercial banks from 20% to 25%.

To provide relief to struggling borrowers, we excluded some loans from being tagged as past due or non-performing and allowed a grace period for loan settlement and restructuring of rediscounted loans.

Thanks to the BSP’s regulatory toolkit and policy reforms, banks continued to actively lend and restructure loans of borrowers during the pandemic.

The level of restructured loans increased 2.6 times to P338.5 billion in September 2021, up from the P130.9 billion in the same period last year. Restructured loans as a proportion to total loan portfolio rose to 3.1% from the 1.2% a year ago.

Bank fees ordered waived

In addition, the central bank suspended certain online banking charges and temporarily waived fees for applications for electronic payments and financial services and PhilPASS fund transfer transactions to provide continued access to financial services during this critical time.

While we have deployed extraordinary measures in response to the unprecedented nature of this crisis, our policy toolkit and regulatory space are far from exhausted. We stand ready to support the country’s continued recovery using the tools at our disposal.

I have said this before and I will say it again: we are one government. We are one Filipino nation.

And we at the BSP shall support all efforts to fight this extraordinary health crisis and keep the economy afloat.

BSP has been and is ready to employ the necessary tools in its arsenal to address the impact of COVID-19 while staying true to its mandate.

Building blocks

However, it bears pointing out that these policy interventions didn’t happen in isolation. Rather, these developments occurred against a backdrop of proactive reforms and policy actions over the years to crisis-proof the financial and economic system.

While the pandemic may have sped up the pace of reform, these structural adjustments were well underway even before COVID-19 hit, allowing the Bangko Sentral to take a longer-term view of the rapidly evolving situation.

Diokno cuts reserve ratios drastically, from 18% to 12%

When I took the helm of the central bank in March 2019, our reserve requirement ratio was among the highest in the world. That year alone, we cut the RRR by a cumulative 400 basis points. This brought our RRR from 18% by the end of 2018 to 14% in 2019, more in line with our neighbors like China’s 13% and Taiwan’s 10.75%. The 200-bp reduction in April 2020 brings our RRR to the current 12%.

Even before the pandemic, I have made it my mission to reduce the RRR to single-digit level and shift to market-based instruments in order to manage overall liquidity.

Likewise, the policy rate, which banks use as reference for their respective lending rates, was as high as 4.75% when I was appointed two years ago. Today, it stands at a record low of 2% in a bid to promote lending to productive sectors of the economy and jumpstart growth.

The path forward

With GDP growing 7.1% in Q3 2021 following a remarkable 12% expansion in the second quarter, the economy appears to have turned a corner and looks set for growth.

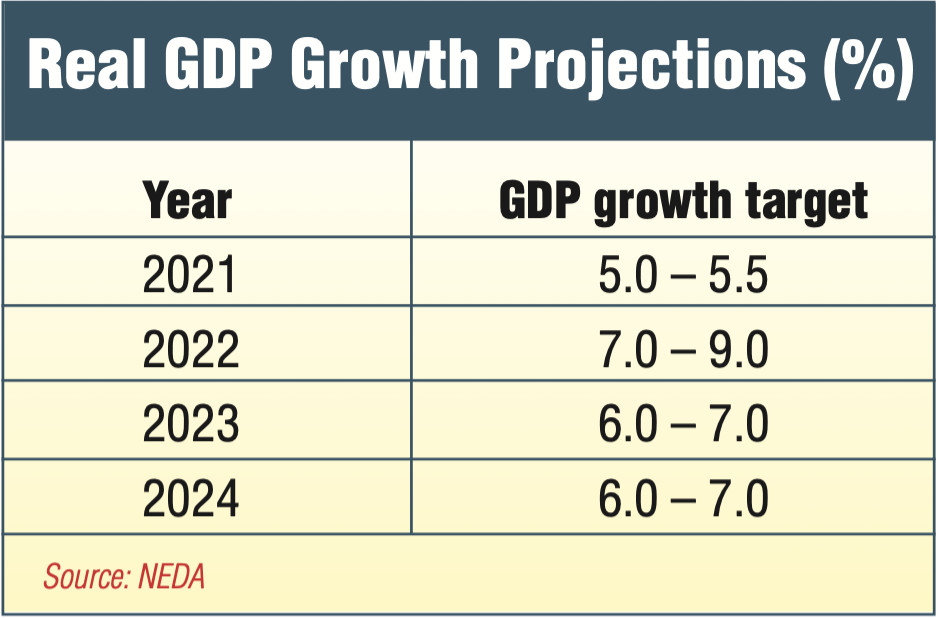

In a sign that recovery is taking a stronger hold, the Development Budget Coordination Committee (DBCC) revised its GDP projection upward for 2021 to 5-5.5% from 4-5%. The DBCC expects the economy to grow by 7-9% in 2022 and 6-7% in 2023 and 2024.

For monetary authorities around the world, the foremost question is whether the elevated inflation is temporary in nature. There are divergent views to this pressing policy question.

Accordingly, a number of central banks chose to tighten monetary policy to keep their economies from overheating while other monetary chiefs opted to take a wait-and-see approach.

Inflation at 3.3% to 4.1%

We expect the latest inflation reading to settle within the 3.3% to 4.1% range in November as higher electricity and LPG prices push the headline figure up. As of November, year-to-date inflation has averaged 4.4% – slightly above the government’s 2-4% target.

Looking ahead, inflation could settle above our target range this year, but we expect it to revert to 3.3% in 2022 and 3.2% in 2023 as the economy normalizes.

While runaway prices continue to concern monetary authorities worldwide, I believe, based on evidence, that the elevated inflation in the Philippines is driven largely by supply-side pressures and does not warrant monetary interventions at this time.

To me, the harm of tightening monetary policy too soon exceeds the harm of moving too late given that the economy is still at a nascent state of recovery.

This crisis, while unprecedented in scale and scope, is unlike other crises in the past.

While previous crises were accompanied by rising interest rates and depreciating peso, aggravated by foreign exchange outflows, the current situation is quite different. This time, interest rates are at a historic low.

Reserves at $107.72 billion

Moreover, our gross international reserves (GIR) remain hefty at $107.72 billion in November.

This level is equivalent to 10.2 months’ worth of goods imports and payments of services and primary income. It also represents 8.7 times the country’s short-term external debt based on original maturity and 5.7 times based on residual maturity.

Thanks to receipts from business process outsourcing firms and remittances from overseas Filipinos, we expect GIR levels to expand even further.

Although major central banks have signaled their intention to tighten policy, we remain focused on domestic developments to inform our policy actions.

The Largest Weekly News and Business Magazine

Timing in winding down pandemic measures

Consistent with BSP’s data-dependent approach to policy-making, the decision on the timing and circumstances under which BSP will unwind its pandemic-induced support measures depend primarily on the evolution of various factors.

Once domestic developments warrant a scale-down of policy support as economic recovery gains traction, we will ensure a smooth transition in winding down its time and state-bound measures.

Central banks around the world are faced with a tough task. If they move to tighten monetary policy prematurely, it could risk holding back the nascent recovery seen thus far.

But if they act too late and fall behind the curve, the economy could overheat and purchasing powers could erode across society, hitting poor households the hardest.

Guiding post: Look at the future

While I choose to maintain our policy settings for now, I always make it a point to look to the future and take a long-term view of the situation.

As a reformist who has served three administrations, I refuse to let the pandemic derail our long-term goals and continue to back structural reforms that would put the Philippines not just on the road to pre-crisis growth but on a sustainable path of development.

Three game-changing laws

Three pieces of game-changing pieces of legislation aimed at liberalizing the economy are already nearing the finish line.

1. The Retail Trade Liberalization Act lowers the minimum paid-up capital for foreign retailers, is already for the President’s signature.

2. The amendments to the 80-year-old Public Service Act have already been approved by Senate in a move that will open up key economic sectors, including telecommunications and airlines.

3. Lastly, both Houses have ratified the final version of amendments to the Foreign Investments Act which will encourage foreign professionals to bring their practice, know-how, and technical expertise to the Philippines.

I am confident that with these game-changing reforms, we can achieve real and lasting impact in a way that affects the ordinary Filipino. After all, the true measure of our effectiveness and relevance as an institution goes beyond our oft-cited mandates of price and financial stability, sound banking supervision, and an efficient payments and settlement system; it is best found in the real economy, in the lives improved because of our actions.

READ FULL ARTICLE HERE: